Stand-alone tail coverage can sometimes be placed after a policy lapse, but only if the gap is short, no claims have been reported, and underwriting can still verify continuous prior acts exposure.

In practice, most carriers treat a lapse as a break in insurability, not just a timing issue. Once a claims-made policy terminates without tail or prior acts coverage in place, the physician is effectively uninsured for past services. Stand-alone tail becomes the only path to restore protection—but availability narrows quickly as time passes.

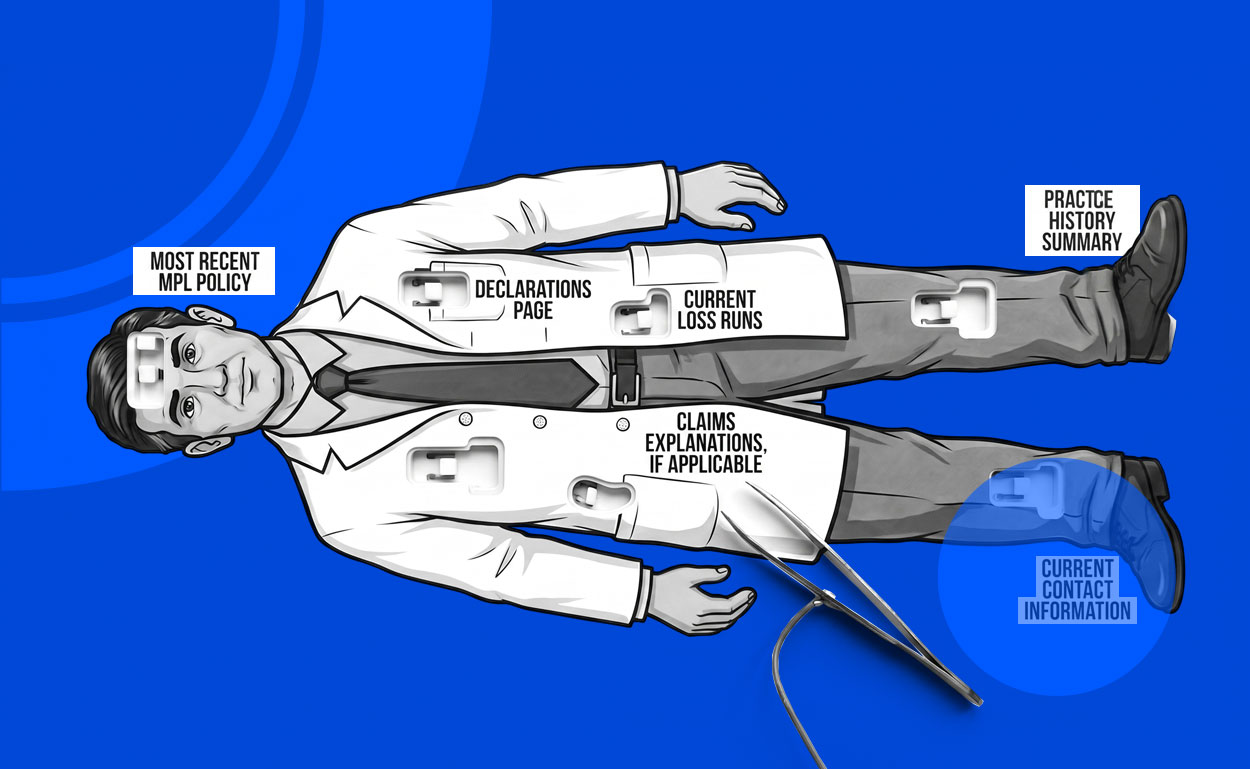

From a placement standpoint, the key variable is not just the length of the lapse, but what occurred during it. Underwriters will immediately assess whether the insured had any knowledge of incidents, whether patient care continued, and whether documentation can support a clean exposure profile.

How Long After a Lapse Can Tail Coverage Be Placed

Stand-alone tail coverage is typically only viable within a narrow window after lapse, often measured in weeks—not months.

Carriers vary, but many will:

- Consider risks within 30–90 days of lapse

- Require detailed loss history confirmation

- Decline outright once the gap becomes difficult to underwrite

Beyond that window, the issue is less about willingness and more about uncertainty. The longer the lapse, the harder it becomes for underwriters to confidently price unknown exposure.

GET THE SUMMIT

Sign up for news and stuff all about the stuff you wanna know about in your sector twice a month.