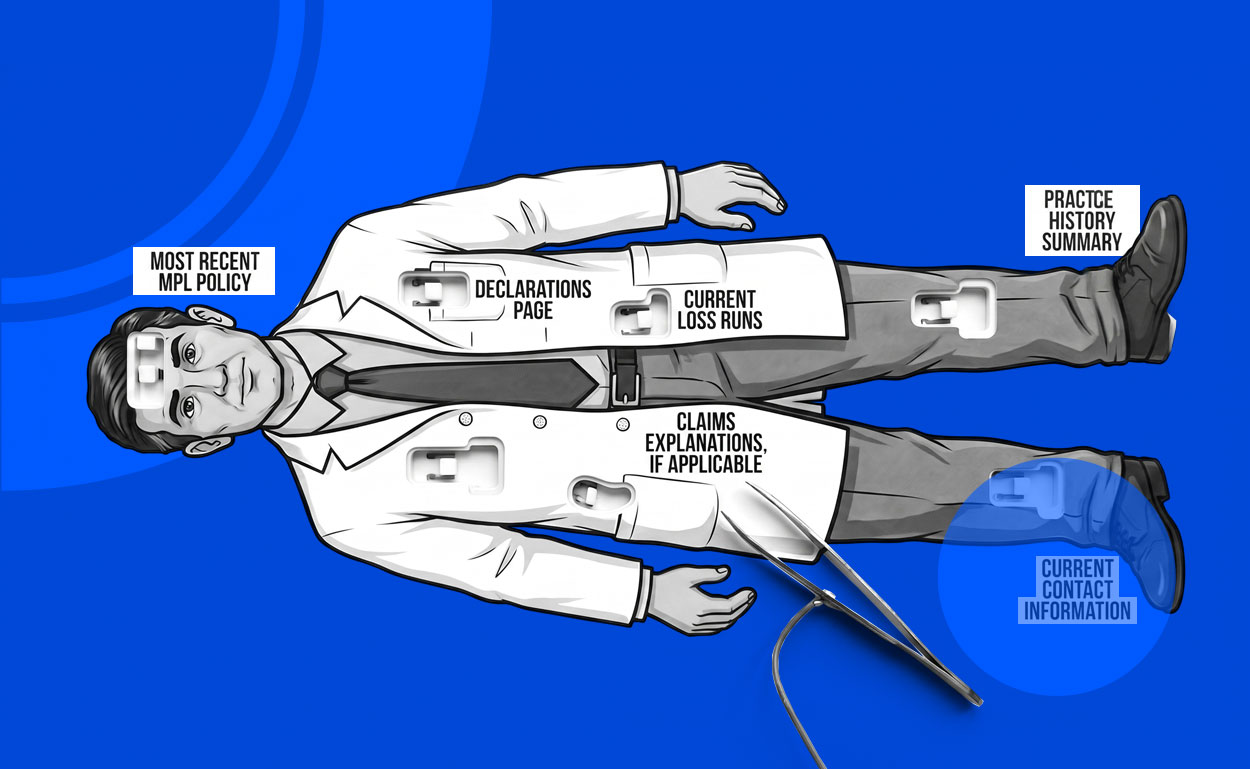

A Growing Market Insurers Can’t Ignore

Integrative and complementary health care isn’t fringe—it’s booming. More than one-third of U.S. adults now turn to treatments like acupuncture, chiropractic care, and naturopathy to manage pain, chronic illness, and overall well-being. Between 2002 and 2022, the use of these approaches nearly doubled. And while clinical acceptance is growing, insurance coverage hasn’t kept pace.

The U.S. complementary and alternative medicine (CAM) market is projected to expand from $28 billion to over $229 billion by 2033. That signals opportunity—not just for providers, but for the brokers and insurers who serve them.

Coverage Gaps—and Client Frustrations

Despite rising demand, traditional carriers often limit or deny coverage for integrative medicine providers. Here’s where things break down:

- Licensing inconsistencies make underwriters wary. A naturopath in Oregon may hold a medical license, while one in New York may not be recognized at all.

- Limited standardization means treatment plans vary dramatically—even within a single discipline.

- Evidence gaps can make it difficult for carriers to quantify outcomes or justify reimbursable procedures.

- High out-of-pocket costs continue to define the patient experience: Americans spend an estimated $30 billion annually on complementary care, most of it uncovered.

Even common services like acupuncture and chiropractic care are subject to visit limits, narrow networks, or administrative hurdles. For providers trying to build sustainable practices—and for patients seeking whole-person care—this is more than a nuisance. It’s a barrier to access.

GET THE SUMMIT

Sign up for news and stuff all about the stuff you wanna know about in your sector twice a month.