Most stand-alone tail coverage applications require prior policy information, loss runs, and basic professional background details so carriers can evaluate the physician's historical liability exposure.

The exact requirements vary by carrier, specialty, and the circumstances surrounding the tail request. In many cases, the underwriting process is relatively straightforward when complete documentation is available. Delays are more commonly caused by missing records than by underwriting concerns.

For retail agents, gathering the right information before approaching the market can significantly improve placement efficiency and help identify potential issues before the submission reaches an underwriter.

What Documents Do Carriers Typically Require?

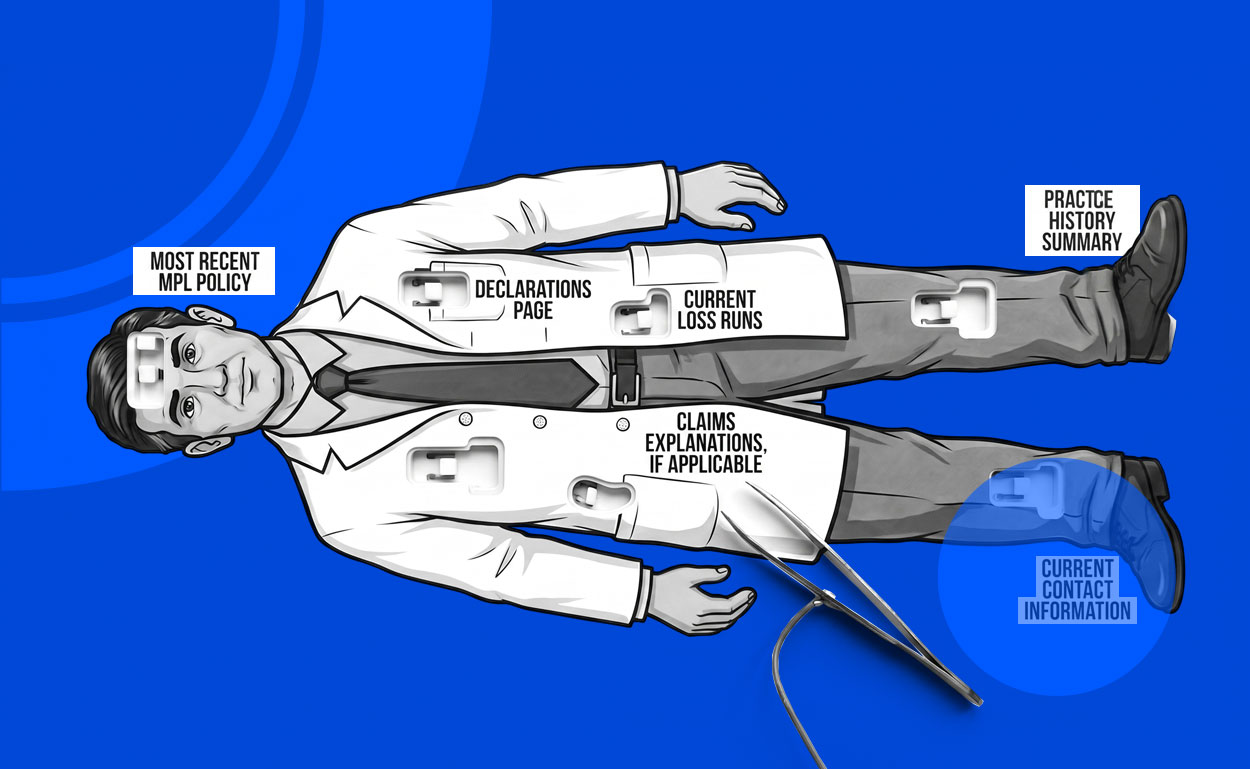

Most stand-alone tail coverage submissions begin with a core set of underwriting documents.

These typically include:

- A completed application

- Current or most recent medical professional liability policy

- Policy declarations page

- Loss runs

- Curriculum vitae or professional resume

- Details regarding any prior claims, if applicable

The purpose of these documents is not simply to verify prior coverage. Underwriters use them to reconstruct the physician's coverage history and evaluate the likelihood of future claims arising from prior professional services.

Why Prior Policy Information Matters

Prior policy information helps carriers determine exactly what period of exposure the stand-alone tail policy will cover.

Because tail coverage protects against claims reported after a claims-made policy ends, underwriters need a clear understanding of policy dates, retroactive dates, limits, and carrier history. Even small discrepancies can create questions during underwriting, particularly when multiple carriers have been involved over time.

For this reason, carriers generally prefer to review actual policy documents rather than relying solely on information entered on an application.

GET THE SUMMIT

Sign up for news and stuff all about the stuff you wanna know about in your sector twice a month.