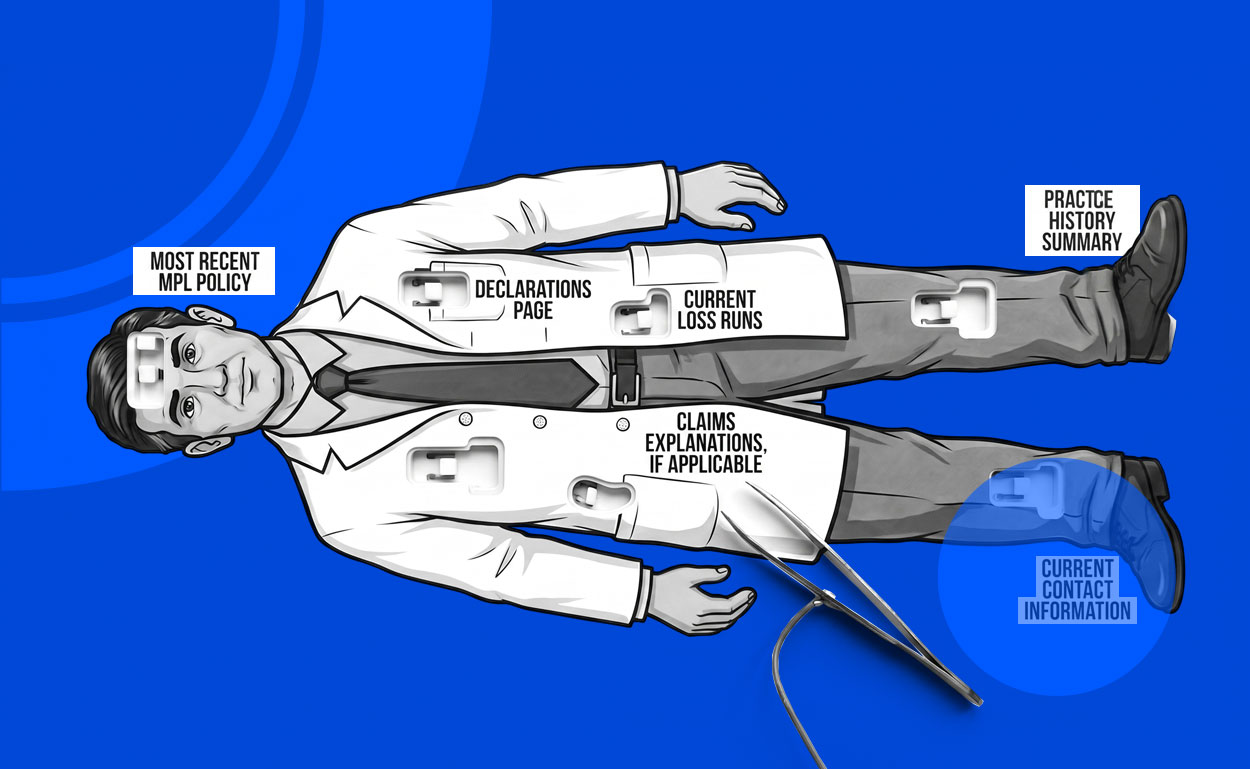

Urgent care has become one of the fastest-growing segments of outpatient medicine, but its growth has brought a distinct professional liability profile. High patient volume, limited clinical history, and broad scopes of service combine to create exposure patterns that differ meaningfully from both primary care and emergency medicine.

For retail medical professional liability agents, urgent care presents a familiar challenge: practices that appear straightforward on paper can carry disproportionate risk if coverage terms and underwriting assumptions fail to reflect how care is actually delivered.

Why Urgent Care Carries Elevated Liability Exposure

Urgent care centers operate in a compressed clinical environment. Providers are expected to assess, diagnose, and treat patients quickly, often with incomplete information and without established patient relationships. This time pressure increases the likelihood of missed diagnoses, delayed referrals, or inadequate follow-up instructions.

At the same time, urgent care centers frequently offer a wide range of services — from basic primary care to imaging, procedures, and occupational medicine — creating variability that complicates underwriting. The combination of speed, breadth, and volume makes urgent care uniquely sensitive to workflow breakdowns.

Common Claim Patterns in Urgent Care

Professional liability claims involving urgent care most often center on diagnostic error. Allegations commonly involve failure to identify serious conditions presenting with non-specific symptoms, such as cardiac events, infections, or fractures that are not initially apparent. Claims may also arise from delayed escalation to emergency care or insufficient discharge instructions.

Procedural claims occur less frequently but can be severe, particularly when laceration repair, splinting, or minor surgical procedures result in complications. As in many outpatient settings, communication failures — including test result follow-up — play a significant role in claim development.

GET THE SUMMIT

Sign up for news and stuff all about the stuff you wanna know about in your sector twice a month.